> CPI is absurd, it only perpetuates consumerism and punishes savers.

Okay okay back up.

The consumer price index is a series of numbers designed to help people understand what dollar-denominated figures mean to ordinary people going about their lives, spending those dollars. If that's "consumerism," well yes, it's a portrait of consumerism.

Many economists, mind you, believe CPI doesn't correct quite enough, and suspect that it overstates the inflation it hopes to measure by around 1%. This is because it tracks the actual prices of a certain "market basket" of goods with specific products in it, and that basket gets out of date, as people substitute products.

But if someone's "punishing savers" and "perpetuating consumerism", it's not the index, and it's not the people compiling the index, and it's not the people trying to make the index more accurate by adjusting for quality. Assign the blame where it's due. You have a beef with the Federal Reserve, and possibly with other agencies or laws which refer to the CPI to make policy.

There's a ridiculous amount of misconception, FUD, and ignorance around inflation / CPI (it doesn't include housing, it overweights entertainent, it exclude food and energy, hedonic adjustments/basket substitutions make everything look artificially cheap)

To professional economists, it can be infuriating to read (I imagine similar as medical professionals reading antivax blogs/comments, or radio engineers reading about dangers of 5G radiation).

I had a good intention once, to write layman exposition to clear most of the misconceptions. But much like the calculation of the CPI itself, it's a lot of work and ultimately not very rewarding. An unfortunate fact is that a very large part of the CPI comes from household survey responses. These are too expensive for non-professionals to reproduce and verify independently, so probably no amount of writing can really convince CPI-doubters.

Is there an index that isn't a 'consumer price index' but a 'cost of living index' instead then? An index that includes the basics of life like food, energy costs, shelter, transport, education, healthcare and some basic consumer goods? I think the issue most have with CPI is it's often sold as a cost of living index by media, politicians and policy makers and it makes people feel unheard as a result.

"My cost of living has doubled but your saying everything is fine since the CPI has only gone up %3!!!" and general 'let them eat cake' style behaviors saying that iPads are 'so much cheaper'[0] is the general feeling I get.

I’ve always wanted to see this + I would love to see two Versions of this, one for a 25th percentile earner, and another for 75th percentile. E.g a) what it costs to rent a modest apartment, drive a Honda Civic, shop at Walmart, have 2.5 kids in public school etc. and B) own a home in a metro area, drive an entry level luxury car, shop at Whole Foods, send kids to private college etc.

It’s my perception that there is not much inflation in some areas of the market (chicken thighs at Kroger) and tons for the “keeping up with the Jones’s” set (organic produce, private school education etc)

My point being that inflation can be quite different based on different baskets of goods / consumption patterns

People constantly cite that CPI excludes things like housing costs, or if we probably dug into it more excludes stuff in strange ways. It's also probably a global thing, some countries do exclude it completely, others do not so it can confuse things:

The CPI does include housing. And my citation for that is the Bureau of Labor Statistics, whose job is to put it together. Here is the document with excruciating detail:

Housing is 42.385%, of which the shelter itself is 33.316%. The rest includes things like "Clocks, lamps, and decorator items" at 0.313%.

That's American data. Maybe the Australian data (your first link) really does exclude it, but the US most certainly does not.

If people think that the basket of goods is skewed, they need to justify that by comparing it against this list. The BLS makes a ton of data available, and it's unreasonable to claim otherwise.

> general 'let them eat cake' style behaviors saying that iPads are 'so much cheaper'

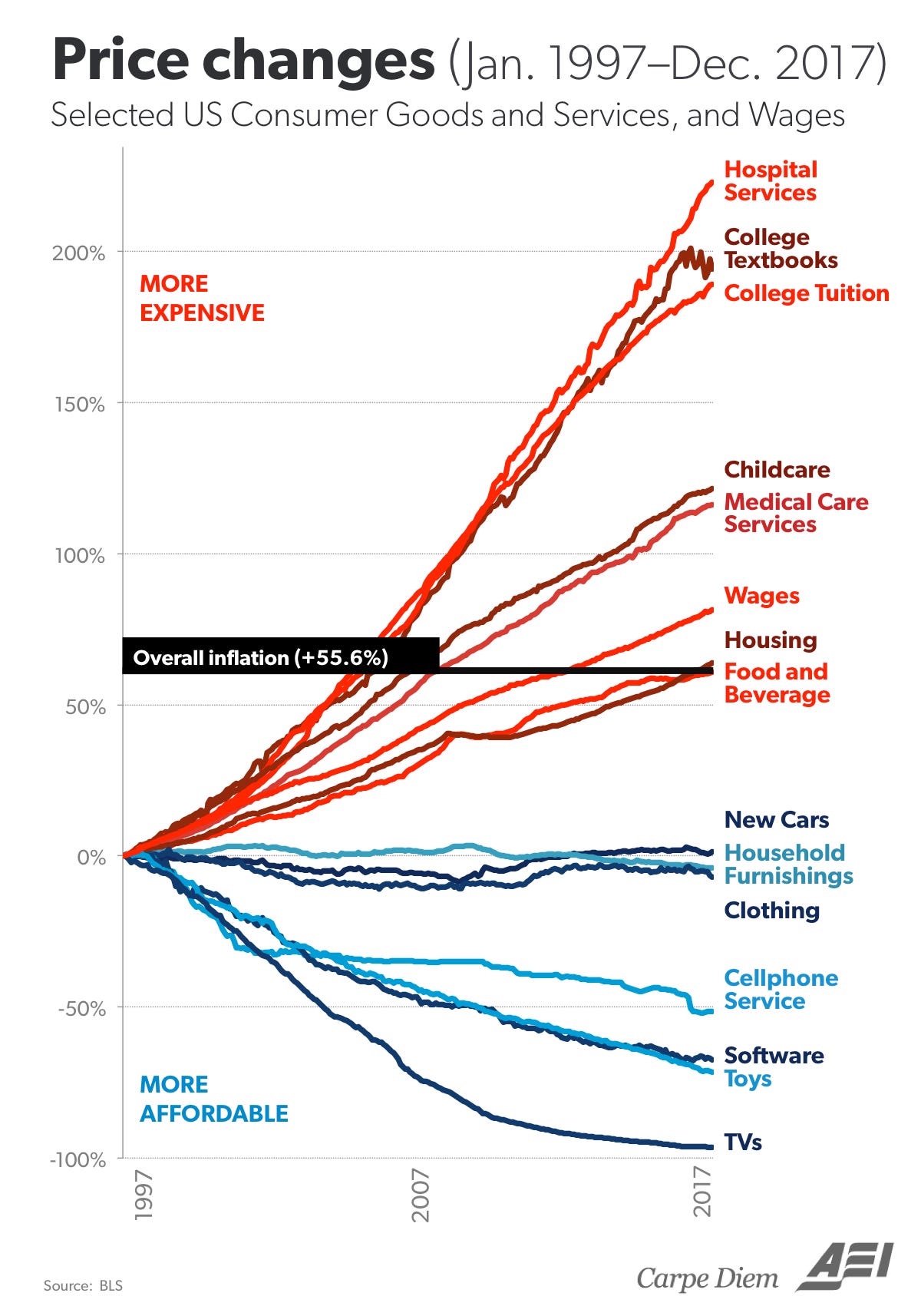

This is a good visualisation of which things got cheaper and others got more expensive, over the last 20 years in the USA. It shows how a "consumer price index" in which, for example, the price of tobacco is weighted at >50% the price of education, can make it seem like it's all okay.

1. The current BLS weights for Education is 3.033%, for Tobacco and smoking products 0.608%, that's 20%, not >50% [1].

2. There are around 20mln Americans in college, versus around 34mln adult smokers. Be careful about peer-group bias: how many of your friends smoke, how many went to college?

It seems like for TVs, it's more that you get a better TV for your money, not that people are spending less on them? A cursory Google search suggests $500-$1,000 was the norm in the 90s, and that seems to be about what people are spending these days too. I can find a nice 24 inch one for $100, but I expect you could find cheaper TVs in the 90s too.

That is a wonderful and very telling graph. Also interesting to note that everything that has becomes cheaper is optional spend (except clothing) that one can do without. Everything above the line which has become more expensive are things which are more necessary.

Maybe the Libertarian in me is coming out when I look at that chart, but it sure seems that the sectors of the economy that increased in price the most are also the most regulated and subsidized.

Without delving into the data, wouldn’t a plausible explanation be that we regulate and/or subsidize those industries _because_ they are the most inflationary? Industries with downward price trends don’t often need consumer protections.

The counter argument is prices come down with increased supply and competition-driven innovation. Regulation inhibits supply. How would regulation make them less inflationary?

My layman understanding of inflation is that it is the measure of change of purchasing power a unit of currency has over time. I think most laymen, including myself, questions how this rather theoretical concept is actually measured in real life. Eg. I think it is a sensible expectation that if inflation was said to be 2% for 20 years then I should be able to buy a house that cost $200K 20 years ago for ~$300K now. This expectation is worlds away from reality which then prompts people to question the way inflation is measured.

I know you wrote that you don't really have the inclination anymore to educate on the topic but I for one would be grateful for any pointers how to explain the above discrepancy?

Good X and Good Y both increase in price over some period of time, but one does by 2% and the other by 4%. What is the true value of inflation? 2% or 4%? Or is it 3%? Or is it 3.5% because you buy one of the goods twice as often as the other? That's a question of first philosophical origins, and there's no "right" answer.

Particularly if one of those is a house and in the period of time mentioned houses not only got more expensive but they changed in character, being more resistant to earthquakes because of reinforced foundations, and because the fire departments built near them got new hoses for their trucks. So if houses were the one that went up by 4% but they also increased in quality, should we "count" them as having gone up by 4%? After all it's not like your money buys you 4% less house since it actually buys you a slightly different house but for 4% more. Now multiply the number of products and dimensions by a thousand or hundred thousand each and we have the true problem of compiling CPI.

> Good X and Good Y both increase in price over some period of time, but one does by 2% and the other by 4%. What is the true value of inflation? 2% or 4%? Or is it 3%? Or is it 3.5% because you buy one of the goods twice as often as the other? That's a question of first philosophical origins, and there's no "right" answer.

Shouldn't the solution basically be how much monthly or yearly does an average consumer spend on x good, and then that is included in the calculation of inflation by that amount.

So if the average consumer spends 30% on housing, then housing should be 30% of the measurement.

Yes. What then should happen when Good Z is invented and grows from 0% to substitute for 25% of Good Y?

How should a measure of inflation track that?

What if Good X becomes half as expensive per unit but people consume twice as much of it as a result? Should that be reflected as a reduction of inflation? If housing per front door goes up by 100% but only up per square foot [or room] by 50%, should the inflation rate of housing be 50%, 75%, or 100%?

TBH looking at my budgets I think this type of argument is missing the point.

Excluding savings, My budget boils down to discretionary and non-discretionary spending. Roughly 1/4th of my budget is fully discretionary and will vary year to year with what I like to do, tracking inflation on the discretionary portion seems like a high difficulty activity which ultimately doesn't matter to my perception of prices.

The remaining 75% of my budget is non-discretionary covering items like

- Housing ~1/4

- Childcare ~1/4

- Food ~1/8

- Non-discretionary expenses (repairs, car, phone, computer, etc. ) ~1/8

I'm fortunate that my healthcare is inexpensive at the moment, but it's pretty straightforward to calculate my future expected health costs and my previous education costs. I'd judge that calculating inflation on the non-discretionary portion of my budget should be trivial, small items like phones/computers simply do not add up to much relative to the big ones like housing, childcare, food, health, and education.

Ironically the CPI seems to focus on the magic basket of goods and not what will actually move the needle for perceived costs by most individuals.

Even discretionary and non discretionary is a contentious item and in a CPI has to be defined.

For example: is TV service discretionary? Is Internet service discretionary? Is broadband Internet access discretionary?

I just checked. Bell TV + Internet is advertised as $120CAD right now. Cell service combined with that add $70CAD. Per month. With taxes on top that's round about $2,620 per year if we are talking Single person household.

Now it depends on where you are and whether you live alone or not and such. In Toronto as a single person at the median income this alone can be 4.5% of your net income. I'd say that moves the needle. I pay less than half of this with a different ISP and cell provider + Netflix. Of course the precise calculations change as we move between cities and provinces as well as single person vs. families etc. as base costs get shared.

The hypothetical single income earner that we are debating would pay an average rent of $2250/mo for a 1-bedroom in Toronto. Roughly 10x the cost of TV, internet, and phone. This cost has risen from ~$1750/mo in 2017 at roughly ~10% per year.

For perspective, our hypothetical individual would be experiencing house price inflation equal to a new TV, phone, and internet bill every year.

Absolutely agreed that there are worse categories than your phone/internet/tv bills. And yet even this relatively small and apparently I Yunsignificant non-discretionary (or was some of it discretionary? Or all of it?) item still makes up 4.5% of your net income. That I still call significant.

Once I have a house the inflation on that also doesn't affect me that much any more (sure, evaluations increase my tax bill - which btw is a NA thing that is irrelevant in Germany for example as long as you have a mortgage) but other items do.

The underlying problem here is that one of our numbers must be wrong. The options I could see are

1. The marginal cost of housing has little to do with what individuals pay in the short-term.

2. The median income earner requires or will require substantial subsidies or raises to keep pace with the increased costs of their home. Roughly 3-4% per year assuming that housing is the only item inflating.

3. Either the median income, median rental, or tv+internet prices we've quoted are wildly off the mark.

I'd bet that #2 is the correct interpretation of the statistics. While option 1 is possible, it hides low-quality substitutions and assumes that one can always make a substitution such as living with parents for longer.

All very fair points. I think one thing that makes a huge difference is whether you rent or own. There's obviously so many nuances to this all.

I realize that we (or at least I am) also mixing up various things, even though I chose to quote a particular city's median income for the example.

If you are renting and your rent goes up 10% that obviously has a large effect. If you have a house and rent goes up 10% you don't care at all. If rent goes up like that, it's probable that house/condo sale prices go up too and you have to pay more in taxes. I bet the increase in taxes makes a smaller hole in your pocket, though I might be completely wrong. But this also depends on whether we stick with the example or move on to other countries, where there's no such thing as separate municipal/school taxes or where rent control is in place.

The problem is laymen care about cost of living, not CPI. But news agencies commonly talk about inflation with CPI rather than an actual cost of living. Which is what matters to people living ordinary lives.

Given this, the answers to your questions should be obvious. The answer, as far as laymen are concerned, is 3.5%. Improvements don't matter either. If we eliminated every car other than a Porsche, as far as laymen are concerned then car inflation went up by around 150%.

>Given this, the answers to your questions should be obvious.

If the answer seems obvious, then the question isn't fully understood, because there are trade-offs involved in CPI calculations.

There's no such thing as a "layman." Different people in different regions experience different CPI. Inflation for all goods in the Northeast might be 2.1% over the past ten years, but could be 1.6% in the South for the same basket. that might not sound like much, but that means that inflation is rising 25% faster in the Northeast.

No matter what you do, CPI at a national level won't accurately reflect any group. People in the South will claim it's way too high, and people in the NE will complain that it's way too low, etc, etc.

If you want real numbers, relevant to your situation, then the BLS provides the ability to calculate your own person CPI based on what you buy and where you live.

Yes, because CPI is a product of both market forces and changes in money supply. The former is not controlled much by anyone, while the latter is controlled by some very rough and not easily predictable knobs held by guys at Fed. Guys at Fed are committed to keep CPI at something like constant 2%, so the must turn these knobs, but for that they need a good feedback as to what their movements are doing.

And sure, they could use something different as a measure of inflation than CPI, but what would that be, and why it would be better than CPI? These questions need to be answered first before we move away from CPI.

The Fed's dual mandate is very important here. And there's some movement toward "automatic QE in case unemployment starts to rise" - https://www.stitcher.com/show/voxs-the-weeds/episode/fix-rec... (Matt Yglesias wonktalks with Claudia Sahm, very recommended)

CPI is very important, but the labor numbers are much better (since they are easier to measure), so CPI might become a secondary (high level, target) metric over time.

The problem with applying CPI to an individual's situation is that nobody is average across several dimensions. One person might live in the midwest an have experienced next to no housing inflation, modest food inflation, and be heavily reliant on gasoline (which has gone down in price over 10 years) due to rural living.

The same person living in Seattle might see housing prices double since they rent, food prices explode, since they live in a gentrifying area where low-cost grocers are replaced by high-end organic ones, and gasoline might not be a huge component of their spend because they drive a beater Prius 15 miles a day.

Those are two people, buying pretty similar things who experience inflation very differently than "average." Luckily, the BLS does provide different CPI figures to account for different groups of people -- for example only looking at inflation data for Seattle -- but people generally never discuss those.

> My layman understanding of inflation is that it is the measure of change of purchasing power a unit of currency has over time.

That's loosely correct; but general inflation is the change in purchasing power for currency buying final consumer goods and services, not assets which are intermediary stores of value. Purchased homes are assets (actual or foregone but using a home you own yourself) rents are consumption expenses.

> I think it is a sensible expectation that if inflation was said to be 2% for 20 years then I should be able to buy a house that cost $200K 20 years ago for ~$300K now

It's not. Specifically, that would be the fallacy of division, even if your basic understanding of inflation was correct. The change of an aggregate is not identical to the change in every subset of the aggregate.

Other already gave good answers. The main part is that

a house is not a consumption product - it is not "consumed" (used up) in a limited timespan, but rather, a bundle of a long-durable part (building) and an ultra-durable asset (land). Pretty much all durable assets have increased in price since the 1980s in tandem with falling interest rates[1]. The cause of the long term decline of interest rates is largely unknown.

The BLS largely circumvents this by using rents, actual rents for renters, and owner equivalent rents (OER) for owners. This is done by asking owners what they think their house would rent for, and using those increases for the housing/shelter component of CPI. Rents (which make up 1/3 of CPI) have increased faster than the general CPI, but not as much as house prices[1], likely because of the interest rate decrease.

There are some other complicating aspects around house prices (city prices increased faster than rural, houses sizes grew while household sizes shrank[3], so part of higher prices is just people buying more). But I believe the main aspects is really falling interests rates. A proper decomposition and attribution of most aspects probably takes months of work, enough for a econ Master theses. That's why I mentioned I don't have the energy for that. Nor do most other bloggers/pop-article writers, so they just go for popular appeal and clicks, by telling you why everything is getting worse and more expensive for you.

Wouldn't it make sense for the basket of goods used to compute CPI to try to blend the impact of rents (which are included) with "affordability" of buying a house (maybe measured as the carrying costs of an average property per month, which would exclude principal payments)?

Otherwise, because rents and house prices don't always move in lockstep, it's hard to measure the buying power of a dollar over time.

When thinking about purchasing power over time or between different cities, I often think of it as "assume I'm buying 1/180th of an average house in that city each month" as part of a representative basket of goods.

Not the parent, but the answer here comes down to two simple things:

1. Home prices are not captured in CPI, only rents.

2. The headline CPI is a national number. Home price inflation has actually been somewhat tame overall in recent history (2-3% per year), but it has been very geographically uneven. Some places have experienced basically no inflation, while others have tons of it.

Here is the graph for home price inflation in the San Francisco region: https://fred.stlouisfed.org/graph/?g=BLdf . You can see that it's often double digits, and certainly much higher than any headline inflation rate.

> Home prices are not captured in CPI, only rents.

Yes, because CPI measures cost of buying service of housing. Usually, if housing prices rise, so do rents, pretty much in accord, so monitoring rents already gives you a good view on housing affordability. The extent to which cost of renting is decoupled from house prices is largely explained by changes in interest rates: lower interest rates make mortgages more affordable, which allows more bidding for houses and pushes prices up. However, this on net doesn’t do much to actual affordability of said house: at low rates, the sticker price on a house might be high, but the mortgage payments will still be low. Conversely, in the 70s and 80s, boomers saw many cheap houses on the market, but at mortgage rates of 10-12+%, these were even less affordable than houses are today.

That’s why CPI only includes rents, to make an apples-to-apples comparison.

> Usually, if housing prices rise, so do rents, pretty much in accord

While this would theoretically make sense, it's not actually very true in the United States. There's a significant speculative aspect to housing in some markets that results in price increases far higher than rents would sustain (this effect is actually more prominent in other markets, e.g. Canada).

I think it actually is very true in the United States, outliers like SF notwithstanding. US as a whole is significantly more like Plano than like SF. Sure, that does little to make Bay Area residents feel better about crazy housing prices they deal with, but theirs is by far not a typical American experience.

You're right that we should probably ignore San Francisco and a few others to portray the typical American experience.

But it's still not obvious why for example Atlanta (22.6x) has almost double the price-to-rent ratio of Milwaukee (12.4x) if not due to speculation. Those both seem like fairly "typical America" cities to me. Would you expect Rent in Atlanta to spike heavily in the coming years? Or is the distinction you're making more about urban vs. suburban? (Since my link is just a mediocre blog, it's not clear if those numbers refer to city or metro area.)

> Home prices are not captured in CPI, only rents.

This is literally correct, but misses the essential feature of the housing issue in CPI: A large component of the housing contribution is "owner's equivalent rent" (OER).

Last I checked (now years ago), there is a survey where BLS essentially polls homeowners with the question "How much would your house rent for?" That number is then used for the OER component of CPI.

As the housing bubble was popping, BLS felt it necessary to explain the divergence between rents and OER [1]. The statistic was an absolute mess then, and I haven't seen any reason why it got cleaned up since, although I have not followed it closely in recent years.

> I think it is a sensible expectation that if inflation was said to be 2% for 20 years then I should be able to buy a house that cost $200K 20 years ago for ~$300K now

Housing is a bit particular because it's a good that's almost always purchased on credit. You'd want to look at the monthly costs of housing (mortgage payment) as opposed to the sticker price, since the total cost that's affordable fluctuates based on the interest rate. Twenty years ago, the interest rate on a 30 year mortgage was about 8%, contrast it with the about 3% rates now.

>My layman understanding of inflation is that it is the measure of change of purchasing power a unit of currency has over time

>I know you wrote that you don't really have the inclination anymore to educate on the topic but I for one would be grateful for any pointers how to explain the above discrepancy?

obvious answer: it's not "price index", it's "consumer price index". First paragraph from wikipedia:

>A consumer price index measures changes in the price level of a weighted average market basket of consumer goods and services purchased by households.

Not an economist either, but I think I can explain that one. CPI is a single rate derived from the change of price in a bunch of goods (houses aren't actually included, as another person noted). A change in CPI tells you nothing about the change in price of a particular good in it; it only tells you how much more expensive those goods are if you bought all of them.

Just as an example, let's say milk and eggs are the only thing on the CPI, and they're both at $2. If milk goes up to $3 and eggs go down to $1, the CPI says there was 0% inflation (assuming they don't adjust for quantity consumed). So rent can go up a lot without affecting the CPI too much, as long as the cost of other goods goes down enough to offset that increase.

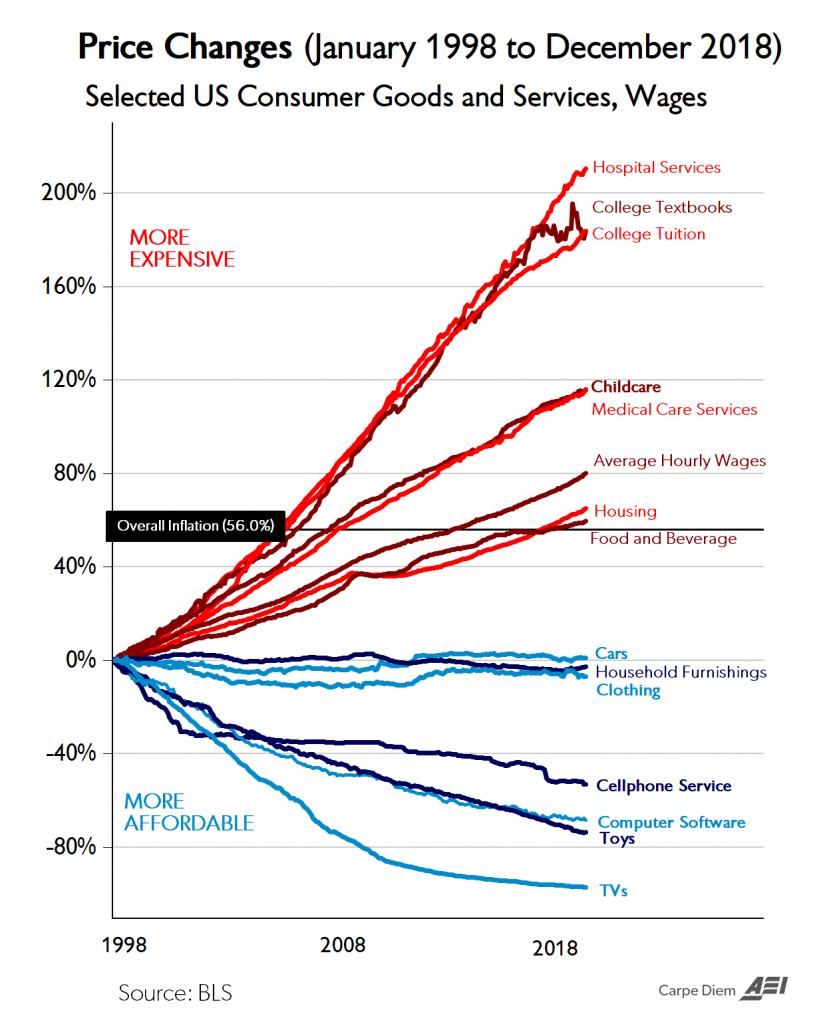

Here's a graph showing inflation of different goods between 1998 and 2018: https://realinvestmentadvice.com/wp-content/uploads/2019/04/... As you can see, a lot of "mandatory" things inflated a lot, but the increase in those costs is offset by the decrease in electronics prices.

The CPI is meant, afaik, to gauge the increase in the cost of living for the "average person". It's useful for driving fiscal policy, but it's not terribly useful to laymen, imo (and that includes myself).

Real wages are more interesting to laymen, I think. Those are effectively wages adjusted over time based on inflation from CPI. Using your housing example again, it doesn't really matter if a house cost $200k 20 years ago and costs $400k now, as long as wages doubled over the same period, all things equal. Inflation is fine (for the purposes of buying a house) as long as wages rise to match that increase.

The reason many people can't buy houses anymore is that real wages have fallen. https://en.wikipedia.org/wiki/Real_wages Wikipedia has some interesting info on that. In an ideal world, inflation decreases the purchasing power of a dollar, but your employer gives you more of them to compensate for that. That never happened for many people.

> Using your housing example again, it doesn't really matter if a house cost $200k 20 years ago and costs $400k now, as long as wages doubled over the same period, all things equal. Inflation is fine (for the purposes of buying a house) as long as wages rise to match that increase.

You are missing one crucial aspect: interest rates. 20 years ago, typical interest rate was 8%, so mortgage payments on $200k house were something like $1400/mo. With today’s rate of something like 3.2%, the payments on $400k house are something like $1700/mo, which is 20% higher. To keep the affordability the same between now and then, the nominal wages need only grow 20%, and if they actually doubled, this would hugely increase affordability.

It doesn't track well with the experience of people on this forum because young professionals tend to live in cities with crushing rental markets, especially Silicon Valley. But the whole country, particularly thoseliving in houses not in New York or California, have a different experience.

it also has real world consequences as CPI is used as a metric for all manners of things, including COLA increases for Social security, as even some private companies.

You forgot the quotes around "economist". Economics is still not science, it's getting closer; but the whole field ignores stuff and deals with spherical cows to simplify complexities.

You know you can be a "professional X" without X being a science, right? It simply means that X is your profession. Some examples of professions that are not sciences: racer, chef, journalist, writer, singer.

Yes, but those professions have agreed upon norms and standards that can be measured.

Did you win, Does it taste good, is it accurate and easy to follow, etc...

Economists are all over the place you an pick and choose different theories to support any Point of view.

I'm sorry, but no, they don't. Out of all of the examples I used, only one has agreed-upon norms and standards that can be measured: racing.

All the other examples I used -- chef, journalist, writer, singer -- can win awards and recognition: Michelin stars, Pulitzer, Hugo, Nebula, Grammy, and such. Those are good indicators of their accomplishments, but that's not the same as having a set of "agreed-upon norms and standards that can be measured".

And if you decide to relax your criteria and say that having those is acceptable, then guess what? There's a Nobel Memorial Prize in Economic Sciences, and a slew of other awards for economists.

Like it or not, studying economics is something that people can and do dedicate their lives to. Would it be better if we had more clarity, transparency, and consensus when it comes to what they do? Absolutely. But dismissing the whole profession out of hand is unhelpful.

I don't dismiss the profession. I dismiss the professionals. They need to provide more proof then identifying as a professional exactly because it is not a science. I also need to understand their biases and agenda.

Honestly it's usually easier to just ignore them and give their opinion no weight greater then anyone else.

I agree with everything you wrote except that last sentence, and that is exactly what I refer to as "dismissing the profession". Understanding their biases and agenda is by no means trivial, or even easy, but it's most likely a lot easier than spending all the time they spent on studying the subject matter.

>The consumer price index is a series of numbers designed to help people understand what dollar-denominated figures mean to ordinary people going about their lives, spending those dollars.

It's done an absolutely terrible job for the past 15 years, for my lifestyle and where I live. I suspect it hasn't reflect many other people's budgets either, hence the common argument of official CPI figures being nonsense.

I don't even have to look at anything other than the changing health insurance premiums/deductibles/co pays/out of pocket maximums to prove it, not to mention real estate, childcare, taxes, and education. It eviscerates any downward effect tech products and grocery prices might have.

My anecdote is as valid as your anecdote. Life got cheaper over the past 15 years, not counting changes in family size.

I used to have insurance co-payment, a deduction from my paycheck, and an unreachable out-of-pocket maximum. All of that has changed.

I used to pay about $1200 rent for a crummy house in a dangerous neighborhood. Now, with a paid-off mortgage, I pay just $266 for property tax on a house that is 3109 square feet on 0.39 acres.

Childcare is my wife, so $0 then and now. Income tax remains $0 due to child deductions. Sales tax is about 7%, relatively unchanged.

Education is a new expense compared to 15 years ago when nobody was in school. If I look back more than 20 years instead, to when I was in college, I can see that college has gotten cheaper. Tuition is a tiny bit lower, but the big change is that tuition and books for the first couple years are now free if you get it done in high school. That cuts the price in half.

This is not to say that I pay less. I now have a huge family. Things are cheaper, but I'm buying much more.

Just so we're clear, here, you've already gone from:

> I can see that college has gotten cheaper

to

> I'm not so sure college has gone up in price

You seem to be good at finding system hacks for your own, and/or proximal cases. But you continue to generalize your own experience(s) in a way that almost certainly doesn't broadly apply.

- Student loan debt at graduation has increased 76% since the Class of 2000, a growth rate that outpaces the rate of inflation by 41%

- After adjusting for inflation, the average student loan debt at graduation has increased 326% since 1970

- Since 2003, the national total student loan debt balance has grown by 602.5%

Of course, tuition prices and student loan stats are different things. But the loan stats make it hard to argue that there is much discounting - in general - of tuition prices

> Many economists, mind you, believe CPI doesn't correct quite enough, and suspect that it overstates the inflation it hopes to measure by around 1%. This is because it tracks the actual prices of a certain "market basket" of goods with specific products in it, and that basket gets out of date, as people substitute products.

Please provide a source to back up this claim, everything I've seen says inflation is /under/-stated, not over. CPI absolutely takes into account substitute products and CPI is not simply tracking a basket of items over time.

> Many economists, mind you, believe CPI doesn't correct quite enough, and suspect that it overstates the inflation it hopes to measure by around 1%. This is because it tracks the actual prices of a certain "market basket" of goods with specific products in it, and that basket gets out of date, as people substitute products.

These substitutions are tricky, if hypothetically a consumer can move from eating fresh local produce to preserved canned produce then it's likely they will make the switch under price pressure when fresh produce increases in cost by 2x. You could calculate CPI based on the new realized purchasing patterns - or you could calculate it based on the desired purchasing pattern.

Basing CPI on realized purchasing behavior will lead to errors in how inflation is perceived or where consumers are trading quality for cost. From a monetary policy perspective ignoring this consumer tradeoff could lead to sudden shifts in CPI when consumers run out of quality substitutions.

I'd argue we've seen this in housing in the major cities where first home prices were excluded for rental equivalent, then rental quality fell in both the amount of space available in a unit as well as the overall quality of the unit. Eventually you hit the wall where quality can't be traded off any longer and you're left with many people who can't legally house themselves.

There have been several eras in computing where a peripheral had a surplus of capability that applications were not making compelling use of. Most especially video cards.

Then one day cards are 'good enough' that someone builds an application that leverages this power, and all of a sudden that becomes the new baseline. Over night you went from having a video card that is three times what you need to a third of what you need.

We might consider availability of seafood to be a given now, due to improvements in food logistics. But it wasn't always the case. For sure strawberries in winter were just not a thing one would buy until relatively recently.

If I wanted vitamin C in February before it would probably be in the form of jam or tomato sauce.

> But if someone's "punishing savers" and "perpetuating consumerism", it's not the index, and it's not the people compiling the index, and it's not the people trying to make the index more accurate by adjusting for quality.

I’ve seen this a lot around the net and I’m honestly and genuinely curious. What drives you to defend the CPI?

He's right, defending the CPI calculation is almost criminal. Many people on fixed incomes that are adjusted based on the CPI are negatively affected. This bogus formula will be conveniently altered to stay under 2% if inflation creeps into the basket of goods being calculated.

Perhaps, but the right way to approach this is to point out the factual errors, rather than making thinly veiled insinuations that his opponent is a shill for the BLS or whatever.

>defending the CPI calculation is almost criminal

Ah yes, because the only possible explanation for why people don't hold the same beliefs as you is because they're acting with malice.

Please don't post insinuations about astroturfing, shilling, brigading, foreign agents and the like. It degrades discussion and is usually mistaken.

Assume good faith.

>Many people on fixed incomes that are adjusted based on the CPI are negatively affected. This bogus formula will be conveniently altered to stay under 2% if inflation creeps into the basket of goods being calculated.

All this does is provide a motive for why CPI might be wrong, but stops short of providing evidence or counter-arguments.

I have no intention of refuting his arguments. I have no strong position on the value of the CPI. OTOH I’ve noticed repeated vociferous defenses of the CPI across various Internet forums which seems out of the ordinary for me, so I’m naturally curious in what drives it. This is not trying to dismiss his argument, I just want to understand from where it’s coming because I think I’m missing something.

I have occasionally come to the defence of CPI in several threads. What drives is usually that the critic shows little knowledge about that the CPI is and/or how it's actually calculated. There are real technical issues with CPI estimations. But forum and blog posts rarely reach beyond the level of "everything I bought/want to buy is getting more expensive faster than the CPI, so it must be bogus".

It triggers me in a similar way, I think, as comments like "my (sisters'/neighbours') kid got really sick after his vaccination, so vaccines are very dangerous". A small number of people really do get sick after (and sometimes even from) vaccines, and probably no amount of research will override their personal experience. But it's a bit disheartening if the level of discourse never rises much above personal experiences.

This is because media and government (in various computations) use CPI when talking about inflation, so it is natural for them to become used interchangeably.

Since CPI doesn't reflect inflation, it is natural to criticize it for failing at that. Maybe it was never meant to reflect inflation, but that seems about as futile as trying to argue for the proper, original meaning of the term "hacker", not what media made it to be.

do you realize all the calculations use CPI?

the bond market is highly manipulated because of that, why have a market then?

why are retail accounts in germany, netherland already negative rates? does that make sense to you?

can banks make money that way? danger of nationalization of banking?

personal beef? no. I thought this is a forum for civil discussion and reasoning?

Whose calculations? The Federal Reserve's calculations? The Federal Reserve has access to a variety of data sources, and while the CPI is the one that gets the press, they also use series like the chained CPI, the producer price index, bond yield curves, unemployment (and not just U3, but things like U6 and the labor force participation rate).

If all you hear about is vanilla CPI, well, that's because you're looking at a newspaper.

Anyway, as I said. You have a beef with the Federal Reserve.

> why are retail accounts in germany, netherland already negative rates?

Public policy, as effected by the European Central Bank. Perhaps you have a beef with them too.

> does that make sense to you?

I mean, it makes sense as in "I understand why they do it", not as in "I think this is a great thing".

> can banks make money that way?

I've read that low interest rates do, in fact, squeeze their profits, though with regards to Germany the "three-pillar" system is crufty and weird and squeezes profits too. For instance, here is this lovely article I saw a while back, whose subhead notes "Low interest rates and the three-pillar system squish profits": https://www.economist.com/finance-and-economics/2019/03/02/c...

> danger of nationalization of banking?

I'm not sure what you're talking about any more. It seems very detached from the Bureau of Labor Statistics, or European equivalent.

Does the Fed look at inflation numbers within individual industries and metro regions?

Here's what I'm worried about: if you look at historical examples like say the 1970s inflation, or the post-Cold-War Warsaw Pact hyperinflations, or the post WW-2 hyperinflations in many European countries, prices didn't rise uniformly. Some industry or some region would experience very large inflation, and then eventually it would get transmitted to that industry's customers, or their suppliers. It's basically a network contagion, spread across the links in the economy.

We're seeing the early stages of this happen right now - that's what the article is about.

Powell's public comments are that "inflation doesn't turn on a dime" and "we're likely to see some localized price increases within certain industries, but no generalized inflation." The thing is - I know from history that the former can be false (particularly in wartime, and shifts from a controlled to a market economy, and the recovery from COVID has aspects of both), and the latter tells me that he's looking at the same data that I am but drawing the opposite conclusion. If 5% of firms are experiencing 30% inflation and the rest are experiencing no inflation, the PPI will read 1.5%. If that 30% inflation is in a core industry though (say food, or energy, or labor) and they pass it along to all their customers, then within 1-2 years you could have 30% inflation across the whole economy without passing through the 2% stage.

It's giving me COVID tingles from last year, where in March your overall risk of getting COVID in the U.S. was about 1:100,000, but your risk in NYC was 30%. Then suddenly your risk in Phoenix was 40%, and your risk in South Dakota was 50%, and then your risk in LA was 30%, and suddenly about 20% of the country has had it.

I don't really have a dog in this fight other than to point out your initial post was neither civil nor reasoned - and included not citations or facts.

I'm starting to understand what you're insinuating I think, but you still haven't made your point.

The European bond market has little connection to the American CPI. European rates are determined by a complex market of futures and interest rate swaps between various banks and markets. Knowing that, negative interest rates make plenty of sense, because interest rates in Europe are relative to other currencies -- unlike in the US, where interest rates are based in a single currency.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Okay okay back up.

The consumer price index is a series of numbers designed to help people understand what dollar-denominated figures mean to ordinary people going about their lives, spending those dollars. If that's "consumerism," well yes, it's a portrait of consumerism.

Many economists, mind you, believe CPI doesn't correct quite enough, and suspect that it overstates the inflation it hopes to measure by around 1%. This is because it tracks the actual prices of a certain "market basket" of goods with specific products in it, and that basket gets out of date, as people substitute products.

But if someone's "punishing savers" and "perpetuating consumerism", it's not the index, and it's not the people compiling the index, and it's not the people trying to make the index more accurate by adjusting for quality. Assign the blame where it's due. You have a beef with the Federal Reserve, and possibly with other agencies or laws which refer to the CPI to make policy.